The first section of the statement of cash flows is described as cash flows from operating activities or shortened to operating activities. Operating activities are also referred to as company operations.

Operating activities are the business activities other than the investing and financial activities.

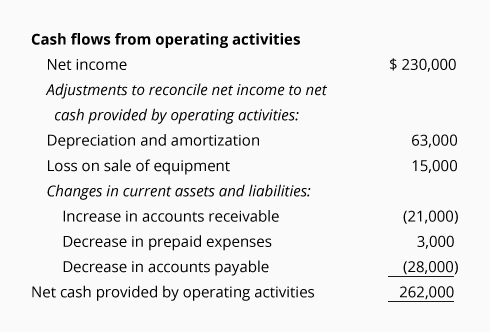

Here is the operating activities section of Example Corporation’s SCF which we will be referring to in our discussion:

Note that the combination of the positive and negative amounts in this section add up to a positive 262,000. Hence, it is described as “Net cash provided by operating activities”. If the amounts had added up to a negative amount, the description would be “Net cash used by operating activities”.

Companies may choose to use either the direct method or the indirect method when preparing the SCF section cash flows from operating activities. However, the indirect method is the dominant method used and the one we will explain.

Under the indirect method, the SCF section cash flows from operating activities begins with the amount of net income, which is taken from the company’s income statement. Since the net income was based on the accrual method of accounting, the amount of net income must be adjusted to the cash amount.

If an adjustment to the amount of net income is in parentheses, it is subtracted from net income. It indicates that the cash amount was less than the related amount on the income statement. Adjustments in parentheses can also be interpreted to be unfavorable for the company’s cash balance.

An adjustment to net income that is not in parentheses is a positive amount, which indicates the cash amount was more than the related amount on the income statement. A positive adjustment can also be interpreted to be favorable for the company’s cash balance.

In the case of Example Corporation, the section cash flows from operating income begins with the company’s net income for the year: $230,000.

A large corporation often has 10 or more adjustments to convert the amount of net income to the amount of cash. However, we will limit our discussion to some of the more common adjustments shown on Example Corporation’s statement of cash flows:

When adjusting a company’s net income for changes in the balances of the current assets, the following may be a helpful guide:

When adjusting a company’s net income for changes in the balances of the current liabilities, the following may be a helpful guide:

The adjustments reported in the operating activities section will be demonstrated in detail in “A Story To Illustrate How Specific Transactions and Account Balances Affect the Cash Flow Statement” in Part 3.

Next, we will discuss the cash flows involving a company’s investing activities.

Please let us know how we can improve this explanation

Submit Feedback No ThanksThe investing activities section of the SCF reports the cash inflows and cash outflows related to the changes that occurred in the noncurrent (long-term) assets section of the balance sheet.

Examples of investing activities include the following:

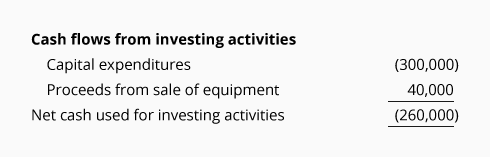

Our discussion uses Example Corporation’s cash flows from investing activities:

Capital expenditures are the amounts spent for acquiring, adding, and/or improving noncurrent assets used in a business. (Large amounts spent for repairing an existing asset are reported as expenses on the current period’s income statement.)

Since the amount spent by Example Corporation for capital expenditures required an outflow of cash, the amount appears in parentheses: (300,000). You can also think of the amount spent as unfavorable for the company’s cash balance and/or cash used.

Proceeds from sale of equipment 40,000 is a positive amount since this is the amount of cash that was received. In other words, the $40,000 was an inflow of cash and therefore favorable for Example Corporation’s cash balance.

(Also see our discussion of Cash Flows from Operating Activities for the reporting of the gains and losses on the sale of noncurrent assets.)

Amounts spent to acquire long-term investments are reported in parentheses, since it required an outflow or use of cash.

The proceeds (cash received) from the sale of long-term investments are reported as positive amounts since the proceeds are favorable for the company’s cash balance.

Please let us know how we can improve this explanation

Submit Feedback No ThanksThe cash inflows and outflows from financing activities are related to the changes in the following balance sheet sections:

Examples of the descriptions and amounts typically reported under cash flows from financing activities include the following:

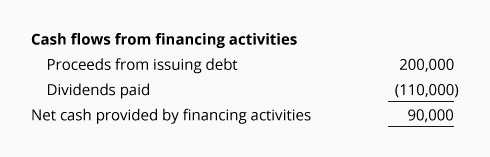

Our discussion of financing activities will use the following section of Example Corporation’s SCF:

Assume that Example Corporation issued a long-term note/loan payable that will come due in three years and received $200,000. As a result, the amount of the company’s long-term liabilities increased, as did its cash balance. Therefore, this inflow of $200,000 is reported as a positive amount in the financing activities section of the SCF.

Next, assume that Example Corporation distributed $110,000 of cash dividends to its stockholders. The $110,000 cash outflow has an unfavorable or negative effect on the company’s cash balance. As a result, the amount will be shown in the financing section of the SCF as (110,000).

When Example Corporation repays its loan, the amount of the principal repayment will appear in parentheses (since it will be an outflow of cash).

If Example Corporation issues additional shares of its common stock, the amount received will be reported as a positive amount.

Please let us know how we can improve this explanation

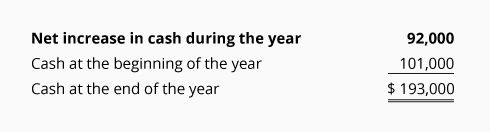

Submit Feedback No ThanksThe three net cash amounts from the operating, investing, and financing activities are combined into the amount often described as net increase (or decrease) in cash during the year.

In Example Corporation the net increase in cash during the year is $92,000 which is the sum of $262,000 + $(260,000) + $90,000.

As was shown in the Example Corporation’s SCF the net increase for the year was added to the beginning cash balance to arrive at the ending cash balance.

The ending cash balance should agree with the amount reported as cash on the company’s December 31, 2023 balance sheet.

Please let us know how we can improve this explanation

Submit Feedback No ThanksSince all transactions cannot be adequately communicated through the relatively few amounts reported on the financial statements, companies are required to have notes to the financial statements.

Some required information for the SCF that will be disclosed in the notes includes significant exchanges that did not involve cash, the amount of interest paid, and the amount of income taxes paid.

Please let us know how we can improve this explanation